Do you know why investing in properties is important nowadays? Your father retired with ₹50 lakhs in savings in 1995. Today, that same amount barely covers a 2 BHK in Lucknow. But if he’d invested it in property back then? He’d be sitting on assets worth ₹2-3 crores. So here’s the real question: Can you afford NOT to invest in property today?

Let me paint you a picture. My uncle bought a 3 BHK in Lucknow in Gomti Nagar for ₹18 lakhs in 2010. Everyone called him foolish for “wasting” money on real estate when FDs were giving 8-9% returns. Fast forward to 2025? That same flat is worth ₹85 lakhs, and he’s collecting ₹18,000 monthly rent. His “foolish” investment gave him 372% returns + passive income for 15 years.

Meanwhile, his friend who put ₹18 lakhs in FDs? Has ₹41 lakhs today. After inflation, barely doubled his money.

This isn’t just my uncle’s story. From flats in Lucknow to villas in Lucknow, from plots in Lucknow to houses in Lucknow — property investment has consistently outperformed traditional investment options while offering something stocks and gold can never give: a roof over your head.

But why is property investment MORE important in 2025 specifically? Let’s dive in.

The Numbers Don’t Lie: India’s Real Estate Boom

India’s real estate market is having a moment. And by moment, I mean a decade-long explosion.

Current Market Size: $482 billion (contributing 7.3% to GDP)

Expected by 2030: $1 trillion Growth Rate: 24% CAGR

To put this in perspective: every major global investor is betting on Indian real estate right now. Foreign investment jumped 37% in 2025’s first half alone. They see what smart domestic investors already know — India’s property market is just getting started.

Why Lucknow Specifically? While metros see steady growth, Tier-2 cities like Lucknow are witnessing explosive appreciation. Properties in developing areas (Faizabad Road, Sultanpur Road) are seeing 20-30% annual returns. Even established areas (Gomti Nagar, Indira Nagar) deliver consistent 10-15% appreciation.

8 Powerful Reasons Property Investment Matters Now

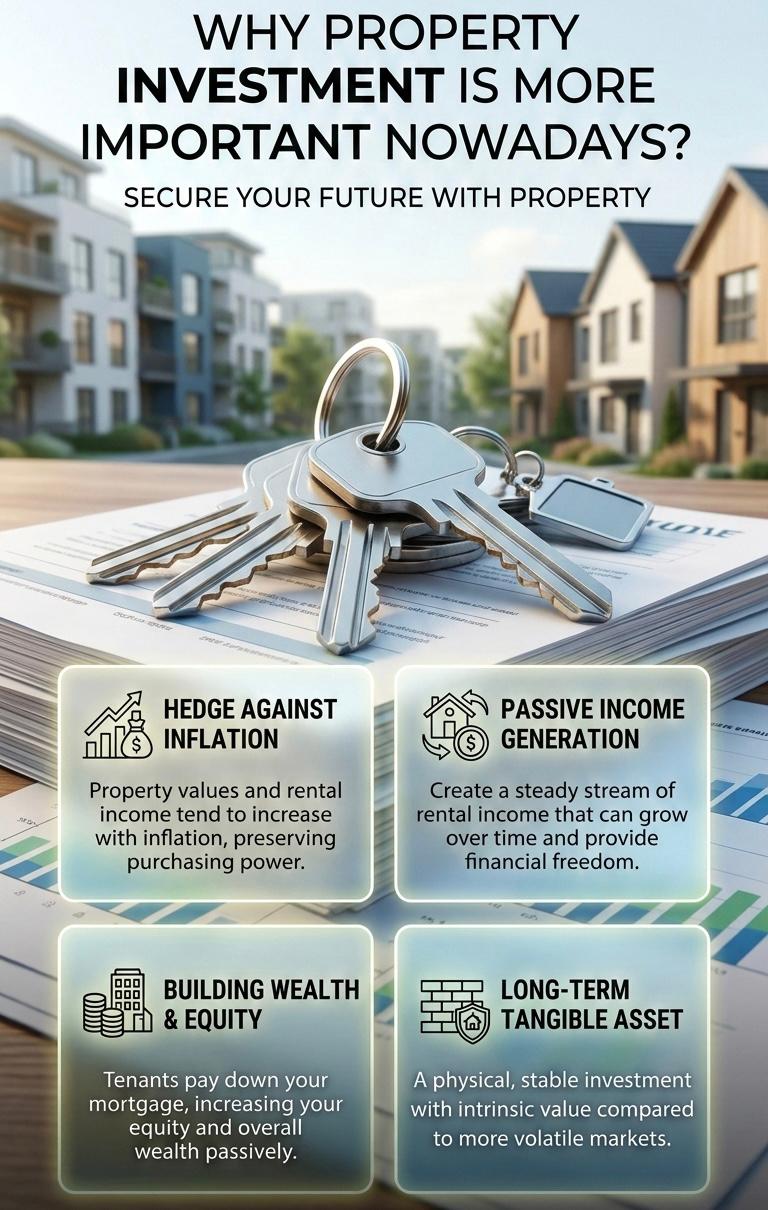

1. Inflation is Eating Your Savings (Property Fights Back)

Your ₹1 lakh FD becomes ₹1.07 lakhs after a year (7% interest). Sounds good? Not when inflation runs at 6-7%. Your real return? Barely 0-1%.

Now look at property: A 2 BHK in Lucknow bought for ₹40 lakhs appreciates to ₹46 lakhs in a year (15% in developing areas). Plus ₹12,000 monthly rent (₹1.44 lakhs annually = 3.6% rental yield).

Total return: 18.6%

And here’s the kicker — as inflation increases, rent increases. Property value increases. You’re not just protected from inflation; you’re profiting from it.

Stocks? They crash. Gold? No cash flow. FDs? Losing to inflation.

Property? The only asset that delivers capital appreciation + rental income + inflation protection simultaneously.

2. The Middle Class is Exploding (Creating Unprecedented Demand)

By 2036, 590 million Indians will live in urban areas (39% of population). That’s 200+ million more people than today needing homes.

Expected demand: $906 billion worth of new homes by 2034.

In Lucknow specifically, migration from smaller UP towns is constant. Every IT professional moving here needs housing. Every family upgrading from joint to nuclear needs space. Every student coming for education needs accommodation.

This isn’t temporary. This is structural, decades-long demand growth.

Whether it’s 3 BHK in Lucknow for families, 4 BHK in Lucknow for joint families, or villas in Lucknow for the affluent — demand will outstrip supply for the next 20 years.

3. Banks Are Making It Easier (And Cheaper) Than Ever

2025 Home Loan Scenario:

- Interest rates: 8.5-9% (down from 10%+ in 2023)

- Loan-to-value: Up to 90% for new properties

- Women co-applicants: Additional 0.05% discount

- Processing fees: Often waived in competitive offers

Tax Benefits Stack Up:

- Section 80C: ₹1.5 lakh deduction on principal

- Section 24(b): ₹2 lakh deduction on interest

- Section 80EEA: Additional ₹1.5 lakh for first-time buyers (new properties)

Real Impact: On a ₹50 lakh loan, you save approximately ₹1-1.2 lakhs annually in taxes alone.

Over 20 years, that’s ₹20-24 lakhs saved.

Plus, forced savings through EMIs builds wealth. Unlike rent (money gone forever), EMI builds equity.

4. Rental Income = Retirement Planning

My colleague bought two 2 BHK in Lucknow properties in 2018 for ₹35 lakhs each. Total investment: ₹70 lakhs.

Today:

- Property value: ₹60 lakhs each (₹1.2 crores total)

- Monthly rent: ₹13,000 each (₹26,000 total)

- Annual rental income: ₹3.12 lakhs

- Capital gain: ₹50 lakhs in 7 years

His plan? In 15 years when he retires, these two properties will:

- Be worth ₹2.5-3 crores (conservatively)

- Generate ₹60,000+ monthly rent (with annual hikes)

- Provide financial security without touching principal

Try doing this with mutual funds or stocks. You sell, you lose the asset. Property? Keeps generating income while appreciating.

5. RERA Changed Everything (Your Money is Safe) https://www.up-rera.in/index

Pre-2016, buying under-construction properties was gambling. Builders delayed projects, diverted funds, disappeared.

Post-RERA (2017):

- Every project registered publicly

- 70% of buyer funds in escrow (can only be used for THAT project)

- Completion timelines enforceable by law

- Builder penalties for delays

- 5-year defect liability period

Real Impact in Lucknow: UP RERA registered 308 projects worth ₹68,328 crores in 2025 alone. Transparency is at an all-time high. Buying flats in Lucknow or houses in Lucknow from RERA registered projects is safer than ever.

What is RERA? Your Complete Shield Against Real Estate Fraud in Lucknow

6. Technology is Democratising Real Estate

2025 isn’t your father’s property market:

Virtual Tours: See 20 properties from your couch before shortlisting 3 for physical visits.

Digital Documentation: Online title verification, instant encumbrance certificates, digital stamp duty payment, e-registration.

Fractional Ownership: Can’t afford a ₹1 crore commercial property? Buy 10% stake. Still get proportional rental income and appreciation.

REITs: Want real estate exposure without buying physical property? Real Estate Investment Trusts let you invest like stocks, earn like property.

PropTech Platforms: Compare prices across localities, check past appreciation, predict future growth, find tenants, manage properties — all on apps.

The barrier to entry is lower than ever. Information is transparent. Frauds are harder to execute.

7. Diversification = Financial Security

Financial advisors recommend 30-40% portfolio allocation to real estate. Why?

Low correlation with other assets:

- Stock market crashes → Property remains stable

- Recession hits → People still need homes

- Currency fluctuates → Real estate holds value

- Geopolitical tensions → Domestic property unaffected

Example: March 2020, COVID hit. Stock market fell 40%. Gold spiked then stabilized. FD rates dropped to 5%.

Property? Paused for 3 months, then resumed growth. Lucknow’s real estate saw 8-10% appreciation in 2020-21 despite pandemic.

Having plots in Lucknow, 2 floor houses in Lucknow, or villas in Lucknow in your portfolio balances risk.

8. Generational Wealth Transfer

This is the part nobody talks about but matters enormously in Indian families.

Your grandfather’s ancestral house in Hazratganj? Priceless today. My friend’s family house bought for ₹2 lakhs in 1980 is now worth ₹4 crores.

Property is the only asset that:

- Survives generations

- Appreciates across decades

- Provides for your children

- Gives your family security

Your stock portfolio might crash before inheritance. Your FDs get divided and spent. But that 3 BHK in Lucknow or those plots in Lucknow? They become your children’s financial foundation.

Where to Invest in Lucknow (2025 Strategy)

For Immediate Returns (Rental Income Focus):

- Gomti Nagar (4-5% yield, stable tenants)

- Indira Nagar (established area, education hub)

- Hazratganj (commercial + residential mix)

Buy: 2 BHK in Lucknow or 3 BHK in Lucknow in these areas

For Long-Term Appreciation (Capital Gain Focus):

- Sultanpur Road (7.5% rental yield + 20-25% appreciation potential)

- Faizabad Road (metro expansion zone, 25-30% growth potential)

- Mohanlalganj (emerging, affordable entry point) Buy: Plots in Lucknow or under-construction flats in Lucknow

For Premium Lifestyle + Investment:

- Sushant Golf City (luxury villas, 15% YoY growth)

- Gomti Nagar Extension (IT professionals, 17.5% appreciation)

Buy: Villas in Lucknow or 4 BHK in Lucknow

Common Investment Mistakes to Avoid

❌ Buying Without Location Research: “Upcoming area” is often “never actually comes up” area

❌ Ignoring Legal Verification: Saving ₹50,000 on lawyer, losing ₹50 lakhs to fraud

❌ Over-Leveraging: EMI shouldn’t exceed 40% of income

❌ Emotional Buying: Fell in love with lobby, ignored seepage issues

❌ Skipping RERA Check: Builder promises vs reality = huge gap

❌ Underestimating Hidden Costs: Budget property price + 25% for total outlay

❌ Timing the Market: Best time to invest was 10 years ago. Second best? Today.

The Bottom Line: Can You Afford to Wait?

Here’s the uncomfortable truth: property prices in Lucknow won’t drop. They’ll fluctuate, yes. Slow down occasionally, yes. But drop significantly? Unlikely.

Why?

- Land is finite (they’re not making more)

- Population is growing

- Urbanisation is accelerating

- Infrastructure is improving

- Demand exceeds supply

Every year you wait is another year of:

- Lost rental income

- Lost appreciation

- Lost tax benefits

- Rising prices making entry harder

That 3 BHK in Lucknow costing ₹70 lakhs today will be ₹85 lakhs in 2 years. Waiting to “save more” often means paying more.

Your Action Plan

If You’re 25-35: Buy one property (even small 2 BHK in Lucknow) on maximum loan. Lock in low rates. Let EMI force you to save. Enjoy tax benefits. Upgrade to bigger property in 10 years using this as down payment.

If You’re 35-50: Already have one home? Buy second property as investment. Rent it out. Let tenants pay EMI. In 15-20 years, you have two fully paid properties worth crores.

If You’re 50+: Focus on rental income. Buy 2-3 smaller properties in high-demand areas. Collect monthly rent. Supplement retirement income. Leave assets for children.

Final Thought

My uncle who bought that 3 BHK in Lucknow for ₹18 lakhs? He’s now advising his son to buy plots in Lucknow in developing areas.

Why? Because he learned the single most important lesson about property investment:

The best time to buy was yesterday. The second best time is today.

Whether you choose flats in Lucknow, houses in Lucknow, villas in Lucknow, or plots in Lucknow — the important thing is to start.

Because in 2035, when property prices have doubled or tripled again, the only regret you’ll have is not buying more in 2025.

Your move. 🏡

Disclaimer: Investment advice is general. Property values fluctuate based on location, market conditions, and timing. Always conduct thorough research, verify legal documents, and consult financial advisors before investing. For more such information visit www.ghargrihasthi.com .